12 min read — China | Trade | EU | Global Europe | Geopolitics

Why China Cannot be Europe’s Alternative to the US

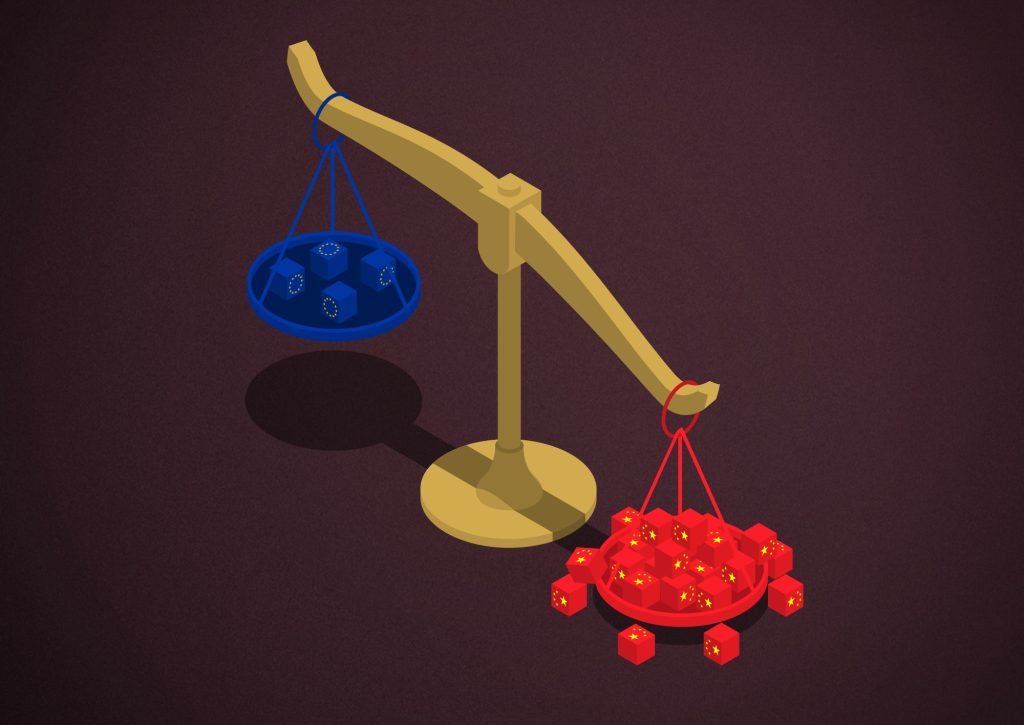

Europe risks trading one dependency for another if it treats China as a shortcut to economic security amid US trade uncertainty.

By Pedro Ursua Marinho — EU Foreign Policy Correspondent

Edited/Reviewed by: Lorist Bown-Dodoo

March 10, 2026 | 16:00

A Warning Based on Facts, Not Ideology

In January 2026, Canadian Prime Minister Mark Carney visited Beijing, being the first Canadian leader to do so since 2017, and emerged speaking optimistically about a “new world order” founded on engagement with China, echoing his previous statements at the World Economic Forum in Davos. The visit resulted in a trade agreement allowing tens of thousands of Chinese electric vehicles into Canada at reduced tariff rates. For some European leaders facing pressure from American tariffs and transactional diplomacy, Carney’s embrace of Beijing might seem like a template worth considering.

It could prove a catastrophic mistake. Europe’s current vulnerabilities, such as American unpredictability, energy dependence and industrial decline are real and urgent. But seeking shelter in Beijing’s orbit would not solve these problems; rather, it risks compounding them with just as dangerous dependencies that, unlike historic American ties, lack shared foundational values and a proven willingness to weaponize economic relationships for political coercion.

The temptation to pivot eastward has never been stronger, particularly as President Trump’s tariff policies create immediate pain for European exporters. But the hard data on China’s economic model, trade practices, and fundamentally anti-Western geopolitical behaviour should make European policymakers re-think a closer friendship with Beijing. This is not an ideological argument about values or political systems, it is a cold assessment of structural economic realities that make deeper engagement with China a path toward dependency, not prosperity.

The Fundamental Problem: China as Mercantilist Power

At the core of China’s economic challenge lies a simple but profound fact: China operates as the world’s biggest mercantilist power, maintaining a trade surplus equivalent to six percent of GDP, larger as a share of both its own and the world economy than the surpluses achieved by Germany and Japan in their boom in the 1970s.

This is not the normal pattern of a mature, balanced trading relationship. In a healthy trading relationship, imports and exports grow in tandem as rising prosperity in one country creates demand for goods from its partners, but China’s model deliberately suppresses domestic consumption to maintain production capacity far beyond what its own population can absorb. Since the COVID-19 pandemic, Chinese exports have risen well above their pre-pandemic trend while goods imports have stagnated below 2021 levels, creating a large and growing trade surplus. The mechanism China employs is heavily subsidizing the industrial and export sector and pairing it with policies that deliberately constrain consumption and boost production. It reflects a policy many analysts refer as ‘deflation export’.

For Europe, this mercantilist model matters enormously. Large surplus nations cannot be sources of economic growth for their trading partners. Period. When a country systematically exports more than it imports, it extracts demand from its partners rather than providing it. Political leaders who think trading with China will solve Europe’s economic challenges are deluding themselves about the the basics of international commerce.

The Structural Roots of China’s Trade Imbalance

Contrary to the United States’ recent change in foreign policy, that can be changed with the next presidency, China’s massive trade surplus is not a temporary phenomenon but the result of deliberate long-term policy choices that show no signs of changing. China’s weak domestic demand stems from its 2021 real estate crisis and state-led manufacturing investment that offers little support to consumption, creating excess capacity that firms redirect toward foreign markets.

The scale is staggering. China’s exports are on track to reach 8 million passenger car exports in 2026, exceeding Japan’s previous record by a significant margin. This export flood is the direct result of overcapacity created by state-directed investment divorced from actual consumer demand, both domestic and international.

French President Emmanuel Macron has branded the trade imbalance with China “unbearable,” calling it “a question of life or death for European industry.” He is right to sound the alarm. The EU’s economic relationship with China is critically unbalanced due to significant asymmetry in market openings, with China’s economic model creating systemic distortions with negative spillovers to trading partners.

The notion that Europe can simply replace American trade with Chinese trade ignores the fundamental difference between the two relationships. The United States, for all its recent concerning behavior, remains a relatively open market for European exports with balanced trade flows. China operates under a fundamentally different model designed to accumulate surpluses at the expense of its trading partners.

Covert Influence and Strategic Threats

China is no ally of Europe’s. China employs covert means to sway European public opinion, funds opposition politicians, sanctions critical voices, organizes spy rings, and conducts sabotage of European economic infrastructure.

For example, The UK’s 2025 China Audit acknowledged that “instances of China’s espionage, interference in our democracy, and the undermining of our economic security have increased in recent years.” British security services, working with thirteen other countries, discovered Chinese state-sponsored hacking of critical national security infrastructure.

The Lithuanian case provides a template for China’s approach. When Lithuania permitted Taiwan to open a diplomatic office in 2021, China banned imports from Lithuania and targeted EU products with Lithuanian inputs, demonstrating Beijing’s willingness to weaponize trade against European states—a policy increasingly mirroring Europe’s recent debacles with Trump. The message to smaller EU member states was clear: standing up to China carries severe economic costs.

China is challenging not just the prosperity of the European Union as a bloc but the fundamental premise of European social democratic societies, namely, that economic prosperity is interconnected with a democratic, inclusive, and egalitarian domestic order. The Chinese industrial model deliberately creates unfair trade practices that undermine this connection.

The Russia Connection: An Unbridgeable Gap

For Europe, there is another fundamental obstacle to closer strategic alignment with China that cannot be overlooked: Ukraine.

China’s economic, diplomatic and arms support for Russia in its war on Ukraine excludes close strategic relations, as top EU leadership regards the war as an existential threat to the continent. Beijing is not a neutral party in Europe’s most serious security crisis since World War II it is actively enabling the aggressor.

European leaders who imagine they can build a strategic partnership with China while China simultaneously supports Russia’s destruction of European security architecture are engaging in dangerous fantasy. The contradiction is absolute.

What Europe Must Do Instead

The evidence is overwhelming: deepening economic ties with China will not solve Europe’s challenges but will create new and more severe dependencies. The question is not whether to trade with China, some level of economic engagement is inevitable and even beneficial, but whether to orient European strategy around closer alignment with Beijing as a response to American unpredictability.

The answer must be an unequivocal no.

Europe needs a fundamentally different approach, one focused on genuine sovereignty rather than substituting one dependency for another. This means above anything, strategic autonomy. Replacing one dependency with another is not strategy, but short-sightedness masquerading as pragmatism. Europe’s challenge is not to choose between Washington and Beijing, but to finally build the economic, industrial, and strategic capabilities that would make such binary choices unnecessary. This requires abandoning the reactive posture that has characterized European policy and embracing genuine strategic autonomy as an imperative, not an aspiration. The path is clear, though demanding:

Building Industrial Capacity.

Strategic autonomy requires first identifying critical sectors and supporting them, and second, building scale as quickly as possible, with industrial and trade policy playing an active role in achieving this autonomy. This means patient capital, targeted demand rules, export credit support, R&D investment, and open standards, applied consistently across Europe.

Strengthening the Single Market.

The best response to increasing world fragmentation and difficulty of trading outside the EU is to deepen the Single Market and eliminate the many remaining barriers to trade between member states. Europe’s 450 million consumers represent enormous, untapped potential if internal barriers can be removed.

Diversification, Not Reorientation.

Europe must diversify its trade relationships across multiple partners rather than pivoting from dependence on America to dependence on China. Europe’s strategic dependencies leave it exposed to foreign influence and interference, limiting its capacity to pursue its agenda in areas such as trade, technology, climate, and beyond without disruption.

Deploying Anti-Coercion Tools.

The EU has created an Anti-Coercion Instrument specifically designed to counter economic pressure from third countries. Among EU member states, some led by France have raised the option of using the Anti-Coercion Instrument adopted in 2023, which allows the EU to hit services, property rights and licences to counter economic coercion coming from foreign countries. These tools must be used when appropriate, not left dormant.

Energy Independence.

In 2024, EU firms faced industrial electricity prices 2.5 times higher than the US and natural gas prices five times higher, contributing to the loss of over 500,000 European manufacturing jobs since 2022. Achieving competitive energy prices through renewable integration and grid stability is essential for European competitiveness.

Coordinated Investment.

The defence, digital and clean transitions are estimated to require an additional €1,200bn per year, nearly half of which depends on public funding. Europe must mobilize both public and private capital at scale through reformed fiscal rules and innovative financing mechanisms.

Mark Carney may speak hopefully of a “new world order” built on engagement with Beijing. But Europeans should recognize this rhetoric for what it is: a dangerous mirage that would lead the continent deeper into dependency at precisely the moment when genuine autonomy has become essential for survival.

Europe’s path forward lies not in pivoting east, nor giving in to the demands of the west, but in finally building the economic, industrial, and strategic capabilities that would make such choices unnecessary. The work is difficult and the investment required is enormous. But it is the only option that leads to genuine sovereignty rather than a new form of subordination.

The facts demand nothing less.

Disclaimer: While Euro Prospects encourages open and free discourse, the opinions expressed in this article are those of the author(s) and do not necessarily reflect the official policy or views of Euro Prospects or its editorial board.

Write and publish your own article on Euro Prospects

Subscribe to our newsletter – stay informed when we publish articles on pressing European affairs.