10 min read — Finance | Economy | Legislation | Policy | EU

Haven’t You Heard? Taxing Cryptocurrencies Is the New Thing!

The old vision of Bitcoin replacing traditional money is losing ground as governments move to tax and regulate crypto like any other asset.

By Antonia Bauk — International Law Correspondent

Edited/Reviewed by: Francesco Bernabeu Fornara

February 19, 2026 | 18:00

Cryptocurrencies are a relatively new topic in finance that gained widespread attention in 2013, with the foundation of Bitcoin in 2009. Cryptocurrencies are digital tokens—that is, they have no physical form as money does. They are a type of digital currency that allows people to make payments directly to each other through a self-contained online system. Cryptocurrencies have no legislated or intrinsic value; they are simply worth what people are willing to pay for them in the market. But as crypto markets expanded, so too has the push for taxation and regulation, leading to the adoption of EU-wide rules such as the Markets in Crypto-Assets Regulation (MiCA). As a result, crypto has increasingly resembled a regulated investment asset rather than a genuine substitute for sovereign currency.

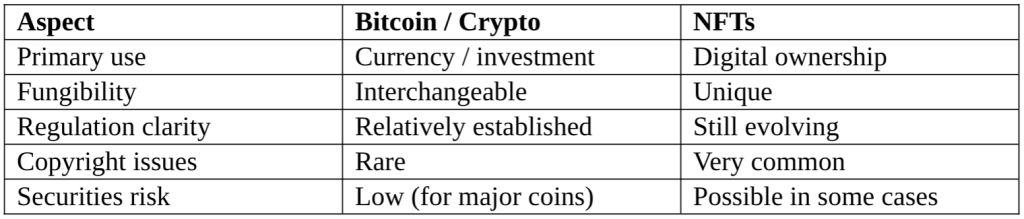

Comparison between NFTs and Bitcoin

Cryptocurrencies and NFTs are both forms of digital assets that can be purchased, sold, or traded using digital currencies like Bitcoin or Ethereum. They may also serve as payment methods and are generally subject to comparable regulations and tax considerations. A key feature of both is their decentralized nature: they operate independently of any central authority, relying instead on blockchain’s distributed ledger technology to record and verify transactions.

Non-Fungible Tokens (NFTs) are unique digital assets that cannot be replaced, exchanged on a one-to-one basis, or divided into smaller equal units. Each NFT exists on a blockchain, where its authenticity, ownership, and transaction history can be permanently verified. Because of these properties, NFTs are commonly used to represent ownership of digital items such as artwork, music, videos, virtual real estate, in-game assets, and even sports collectibles. While their uniqueness gives them value as proof of originality and scarcity in the digital world, their variety has become a real sticking point for regulators.

Bitcoin, by contrast, is a decentralized digital currency rather than a collectible asset. It is also recorded on a blockchain, but unlike NFTs, each unit of Bitcoin is fungible—meaning one Bitcoin has the same value and can be exchanged equally for another. Bitcoin was designed primarily as a peer-to-peer payment system, allowing users to send and receive money without relying on banks or central authorities. It can be used to purchase goods and services, transferred across borders, or held as a store of value. In many cases, cryptocurrencies such as Bitcoin (and more commonly Ethereum) are used to buy, sell, or trade NFTs on online marketplaces.

In summary, while both NFTs and Bitcoin rely on blockchain technology and decentralization, they serve very different purposes: NFTs represent ownership of unique digital items, whereas Bitcoin functions as a digital form of money used for transactions and value transfer.

From idealised currency to just another asset: the legal and tax view on cryptocurrencies

The legal and tax treatment of NFTs and cryptocurrencies such as Bitcoin and Ethereum reflects the broader challenge regulators face in adapting traditional legal frameworks to rapidly evolving digital technologies. Although both asset types are built on blockchain infrastructure and share features such as decentralization and global accessibility, authorities increasingly distinguish between them based on their economic function, risk profile, and real-world use.

From a legal standpoint, cryptocurrencies are now widely recognized across the European Union as lawful digital assets, though they are not considered legal tender like the euro or US dollar is. This distinction is crucial: while individuals may use cryptocurrencies for payments, investments, or value storage, governments do not guarantee their value or accept them for mandatory payments such as taxes.

The introduction of the European Union’s Markets in Crypto-Assets (MiCA) Regulation marks a significant step toward harmonizing rules across EU member states. By imposing licensing requirements, transparency obligations, and consumer safeguards on crypto service providers, MiCA aims to reduce fraud and systemic risks while fostering innovation in financial technology. That said, the decentralized and irreversible nature of blockchain transactions continues to pose challenges for consumer protection, dispute resolution, and financial stability oversight.

NFTs present a more complex regulatory picture. Unlike Bitcoin, they are not a single, uniform asset class. Instead, they function as digital certificates of ownership that can represent anything from artwork and collectibles to access rights or investment interests. Consequently, regulators must assess NFTs almost on a case-by-case basis. While most NFTs are treated as digital collectibles, some may fall under financial regulation if they promise profit participation or resemble securities—particularly when fractionalized or marketed as investment products.

What’s more, legal concerns surrounding NFTs frequently extend beyond financial regulation into intellectual property law, as ownership of a token does not automatically confer copyright or usage rights over the underlying content. This creates potential disputes regarding licensing, authenticity, and platform responsibility. It highlights an expanding and unexplored area of digital regulation:, the intersection between technology law and traditional property rights.

Tax treatment further illustrates the convergence and divergence between these assets. In most jurisdictions both cryptocurrencies and NFTs are treated as taxable property. Capital gains taxation applies when assets are sold, exchanged, or used for purchases at a profit, reinforcing the view that digital assets function as investments rather than currency substitutes. Importantly, taxation is triggered not only by conversion into fiat money but also by crypto-to-crypto trades or the acquisition of goods and services, reflecting the principle that economic gain occurs whenever value is realized.

In other words, while Europeans may experience a form of “profit” when the euro’s value appreciates, their euros are not taxed on that gain. By contrast, although cryptocurrencies can similarly fluctuate in value and function like currency in payments, regulators now seem intent on taxing those increases in value at the moment they are sold or used in transactions—just like stocks or real estate. As a result, the days when crypto proponents envisioned a future in which Bitcoin would replace centralized currencies appears to be fading.

This approach can create complex record-keeping obligations for taxpayers, especially given the volatility of crypto markets and the frequency of transactions.

Income taxation introduces another layer of complexity. When digital assets are earned—through mining, staking, employment compensation, freelance work, or NFT creation—they are typically treated as ordinary income rather than capital gains. This distinction is significant because income tax rates are often higher and apply regardless of whether the assets are later sold. For NFT creators in particular, revenue from primary sales is usually considered business income, underscoring that participation in digital markets can constitute entrepreneurial activity rather than passive investment.

Value-added tax (VAT) rules demonstrate how existing tax systems adapt to new payment technologies without fundamentally altering underlying principles. While the exchange of cryptocurrency itself is generally VAT-exempt in the EU, goods and services purchased with crypto remain taxable in the same manner as conventional transactions.

Similarly, NFT sales may attract VAT when classified as digital services, particularly in commercial contexts. This ensures fiscal neutrality: the tax outcome should not depend on whether payment is made in euros or in digital assets. The most important legal precedent for the EU is the CJEU Hedqvist case (C-264/14). The exchange of crypto and fiat is VAT-exempt, argued the Court, and crypto is treated similarly to traditional currency for VAT purposes.

Conclusion

Overall, the evolving legal and tax framework for cryptocurrencies and NFTs reveals a broader trend toward normalization. Rather than treating these technologies as entirely new categories requiring wholly novel laws, regulators increasingly integrate them into existing systems governing property, finance, taxation, and consumer protection.

However, whether regulation can keep pace with technological innovation is becoming ever more unclear, especially for hybrid or emerging use cases. As adoption grows, further refinement of legal definitions, cross-border coordination, and enforcement mechanisms will be necessary to balance innovation with financial stability, investor protection, and equitable taxation.

Disclaimer: While Euro Prospects encourages open and free discourse, the opinions expressed in this article are those of the author(s) and do not necessarily reflect the official policy or views of Euro Prospects or its editorial board.

Write and publish your own article on Euro Prospects

Subscribe to our newsletter – stay informed when we publish articles on pressing European affairs.