12 min read — Analysis | BRICS | China | Economy

BRICS by 2049: A China-Dependent Counter to the West?

As China’s economy decelerates, concern lingers among BRICS members over whether its Chinese powerhouse can rally the bloc and revive growth to sustain the bloc’s future relevance.

By Francesco Bernabeu Fornara — Editor-in-Chief

December 11, 2024 | 10:30

Introduction

By 2001’s year-end, Goldman Sachs––an archetype of Western financial dominance—ironically became the first to theorise and coin the term “BRIC”, a group of four emerging economies—Brazil, Russia, India, and China—destined to counterweigh Western economic hegemony. Eight years later, the term was appropriated and the organisation formally conceived, with South Africa joining a year later at China’s request, adjusting the acronym to “BRICS”. Since then, despite having no formal charter, the bloc has sought to become an advocate for the Global South and an alternative to the Western-led world order. Accordingly, its members have gradually consolidated their economic policies, created alternative financial systems, and facilitated intra-bloc trade. Today, following its six-member enlargement, the organisation accounts for 46% of the global population and 35% of world GDP (in PPP), surpassing the G7 half a decade ago.

A Faltering Chinese Economy?

Yet, despite BRICS’ impressive economic growth, nearly all of it is attributable to China’s exponential rise, with all other members’ growth remaining largely flat, bar India’s only-recent accelerated expansion. China moreover represents more than a third of BRICS’ combined GDP. And of the sevenfold increase in intra-BRICS trade since 2007, China’s share has represented half of it, with other members’ bilateral trade growth remaining low. This, paired with China’s recent geopolitical assertiveness, has underscored the reliance BRICS’ relevance has to China’s leadership and especially its continued economic growth.

Domestically, however, China’s ‘economic miracle’ of the past four decades, typified by above-8% GDP growth, ‘rapid industrialisation, export expansion, and large-scale infrastructure investment’, is decelerating, spelling concern for a China-dependent BRICS. One of China’s direst challenges—its aging population—exacerbated by its one-child policy, has translated into a gradually diminishing workforce, reducing productivity and hampering its export-driven economy as its familiar competitive edge through cheap manufacturing erodes—a challenge compounded by an exhaust of rural surplus labor from China’s hyper-urbanisation of the past decades. While advanced economies traditionally remedy such slowdowns by shifting to consumer-driven economies—the so-called ‘middle-income challenge’— even here China is facing obstacles, aggravated by the 2008 financial crisis and the pandemic’s aftereffects. In addition to the pressures an aging population places on sustaining social services, a larger elderly citizenry equally means reduced consumption as older people tend to spend less. With BRICS dependent on a steady Chinese manufacturing workforce and especially a high consumption of its members’ exports, the Chinese Communist Party (CCP) is seeking new avenues, such as future industries including AI and green technology, to retain steady growth.

An (In)Cohesive BRICS?

Adding to BRICS’ difficulties is its heterogenous membership, exemplified by an India-China tension. With the bloc’s decision-making based on consensus, BRICS’ effectiveness in dethroning Western hegemony largely depends on its cohesiveness. China’s desire to expand the organisation with Global South countries is likely not to help, not least because of India’s reluctance to cede influence. For reasons such as these over BRICS’ incoherence, Western media has often dismissed the bloc’s relevance, but the fact that so much of the developing world has rushed to voice their candidacy should not by overlooked. Still, while China and India managed to settle their border tensions with the Line of Actual Control agreement signed in October 2024, underlying divergences in their preferred future global order remain. While New Delhi is satisfied with BRICS offering it an elevated status on the global stage where the West acknowledges the conditionality of its support, Beijing’s aspirations go further, envisaging a bloc that supersedes Western-dominated institutions, is integrated with its Belt and Road Initiative (BRI), and offers a financial alternative for countries of the Global South. Indeed, the clash between anti-western states like China and Russia and non-aligned members like India and Brazil will inarguably epitomise BRICS’ cohesiveness and hence China’s global influence from it.

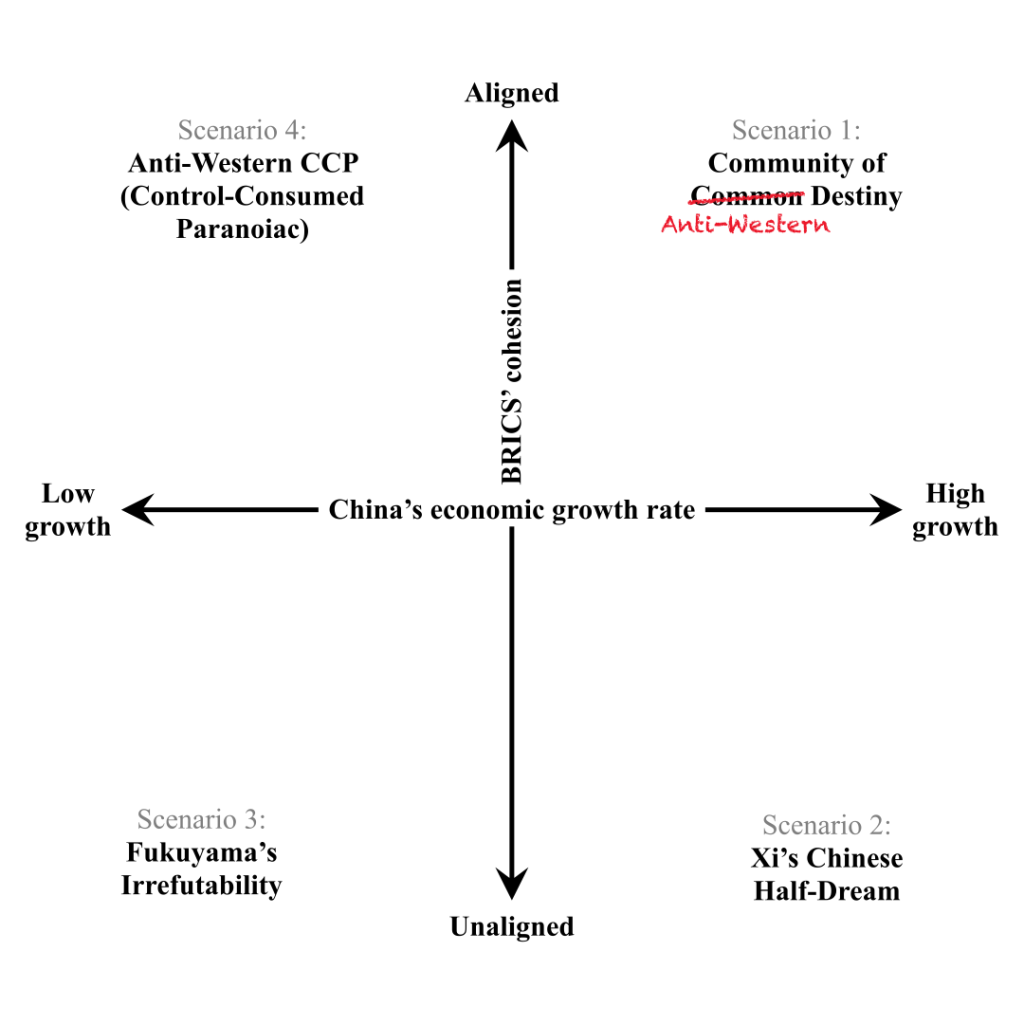

The Two Axes

By 2049—the centenary of the People’s Republic of China—Xi is determined to transform the country into a fully developed nation and ‘pioneering global influence’, two goals inextricably linked with the aforementioned factors which condition BRICS’ future: (1) China’s economic growth and (2) the blocs’ cohesiveness, respectively. It is for this reason that these two factors are chosen as axes in predicting China’s 2049 (geopolitical) future through BRICS, as shown below.

Each corner hence represents a different prospect for BRICS in 2049 dependent on the future of the two above-mentioned factors. Were China to maladminister its underlying economic challenges and BRICS to fail to unify, the bloc’s relevance and China’s influence will likely decay (scenario 3). Were China to reinvigorate its economy but fail to reach cohesion within BRICS, Xi’s 2049 ‘Chinese Dream’ of becoming a ‘pioneering global influence’ may not reach its greatest fruition (scenario 2). Were China to continue its economic deceleration, giving other members like India ability to successfully lead the bloc, BRICS may remain relevant but not under Chinese dominance (scenario 4). Were China, as is this paper’s proposition, to adequately remedy its economic challenges and rally the bloc’s members under its direction, BRICS and China may likely realise Xi’s aspirations, posing the greatest threat to Western dominance in global governance (scenario 1).

Daunting, but Acknowledged Challenges (Scenario 1: High Growth)

Despite facing formidable economic obstacles, the CCP is nonetheless acutely aware of the challenges China faces. In addressing its aging population, efforts are underway to increase retirement age and ‘foster a birth-friendly social atmosphere’ through ‘13 targeted measures’ including subsidies, tax reliefs, assisted reproductive technologies, and ensuring geographic equity of paediatric resources, as per China’s State Council. And as labour costs rise, China’s ‘Made in China 2025’ policy of modernising its manufacturing base in ten high-tech sectors through automation is providing an ideal remedy to its diminishing workforce, keeping productivity high, costs low, and the economy competitive in future industries like AI, electric vehicles, and telecommunications.

In addressing China’s mounting debt which threatens to constrict BRICS’ growing intra-trade, the CCP has unveiled a $1.4 trillion debt package destined to tackle flagging economic growth through ‘debt-swaps’ with highly indebted municipalities. Though still restrictive, China has also been cautiously liberalising its lucrative capital markets to foreign investment, cultivating a fertile supply of private capital for innovative projects and debt repayment. This was met with announcements of trade-boosting measures including expanding export credit insurance and improving cross-border e-commerce development, reported CCTV.

Indeed, were the CCP to continue the acknowledgment of the country’s economic challenges, exemplified in the Politburo’s recent September meeting readout, China has the resources to effectively transform its economy by 2049 through: (1) addressing the negative effects of demographic shifts via automation and incentivising fertility; (2) leveraging its hyper-urbanisation as an advantage for increased consumption; (3) maintaining competitiveness through future technologies; and (4) facilitating cross-border BRICS trade.

Achieving Economic, Rather Than Political Alignment? (Scenario 1: Aligned BRICS)

BRICS faces undeniable internal divides. While the bloc’s political unity has grown, symbolised by coordinated UN voting decisions in areas concerning Xinjiang, Ukraine, and Israel-Palestine, cohesion on more mutually more sensitive positions are unlikely to occur, particularly as BRICS further expands. What does align all members, however, is their determination to rebalance representation within the Western-led world order, particularly within financial institutions like the International Monetary Fund (IMF), the World Bank, and the financial-telecommunication platform SWIFT.

In such areas, the bloc has unequivocally coalesced. In 2014, the New Development Bank (NDB) was established, complementing China’s BRI and providing an alternative funding source for emerging economies. And with the NDB loaning on terms far more lenient than the IMF or World Bank on areas like market liberalisation and human rights, similar future financial initiatives by 2049 may prove to be effective rallying policies for a group increasingly considered an alliance of undemocratic countries, backed by cash-rich states like the UAE and (potentially) Saudi Arabia, in a progressively more autocratic world.

As for monetary cohesion, BRICS members are increasingly aligned in their will to dethrone the US dollar as the world’s standard trading currency, with the NDB having issued one-fifth of their loans in Chinese yuan and the bloc launching BRICSpay as an alternative to the dollar-based SWIFT since Russia’s exclusion thereof following Western sanctions. Similar initiatives have also been established, including the Think Tank Network for Finance, BRICS Clear, the Payment Task Force, the BRICS Grain Exchange, and the Contingent Reserve Arrangement.

Indeed, while BRICS is unlikely to coalesce on contentious political positions, an alignment founded on superseding Western-dominated financial global governance, typified by initiatives like the NDB and BRICSpay, will most likely deepen by 2049.

Conclusion and Counter-Arguments

Joined, a reinvigorated Chinese economy and a financially aligned BRICS will prove a credible threat to the Western-led world order by 2049—though this is admittedly far from certain.

Even if successful, China’s demographic policies are unlikely to offer immediate relief from still-to-grow budgetary pressures caused by low fertility rates and miscalculated birth restrictions. Indeed, China’s aging problem has only just started, with expected proportions of the nonworking-age—that is, low-spending—Chinese citizenry reaching 66 percent by 2049, spelling concern among BRICS members relying on China’s ability to sustain import consumption. Compounding this concern is the impact of the country’s dismaying private sector debt which may undermine China’s dominance within the bloc as Chinese companies divert into servicing debt than buying imports to start new projects. This is especially worrisome given the particularly-indebted property sector has traditionally driven China’s exponential growth through unprecedented state-funded infrastructure investment. Not ameliorating the dept situation is China’s paternalistic model of incentivising innovation through massive lending and ‘picking the winner’, likely not to change given the CCP’s growing restrictiveness and reluctance to expand market decentralisation.

Despite this, research joining Peking University and the Brookings Institute has found that if hyper-urbanisation was effectively remedied through automation, as seen in the “Made in China” programme, the UN-projected 80% urbanisation by 2049 could actually be leveraged to mitigate weakening consumption as urbanites buy twice as much as rural people—hence preserving a reliable pool of BRICS consumers.

Disclaimer: While Euro Prospects encourages open and free discourse, the opinions expressed in this article are those of the author(s) and do not necessarily reflect the official policy or views of Euro Prospects or its editorial board.

Write and publish your own article on Euro Prospects

Subscribe to our newsletter – stay informed when we publish articles on pressing European affairs.