12 min read — Legislation | EU | Policy | Economy

Drafting the Dream: Can the EU Build a Savings and Investments Union?

Can the EU turn its €10 trillion in idle savings into the foundation of a true Savings and Investments Union—and finally gain financial independence from U.S. capital markets?

At a time of troubled market fluctuations, caused by uncertainty in what had been a commercially friendly country, now put into question due to a tariff war, the need for financial independence has risen to the top of priorities for the European Union, as the need to strengthen the European economy becomes imperative.

The European Commission has acknowledged the disparities between the investment opportunities available in the US and EU, with Maria Luís Albuquerque, the Commissioner for Financial Services and the Savings and Investments Union, navigating across Europe to interact with all types of stakeholders and hear their feedback on the Savings and Investments Union (SIU) being prepared in order to unlock the true potential of the European financial markets and reduce both the dependency, but also influence, of the american capital.

Comparative analysis

In recent years, the distance between the capitalization of the US stock market and the European counterpart has increased, having reached a historical ratio of 3 to 1 in 2024, exemplified by the stark difference of value between Europe’s Stoxx 600 and the US S&P 500, with a clear majority of most expensive companies in the world being based in the US and lacking any European company in the top 10. However, this trend saw a reversal since even before the tariff turmoil triggered by the US administration, with EU-focused indexes gaining as the US counterparts saw decreases, with data indicating the concentration of US equity liquidity on the commonly referred mega-capitalization stocks (firms with market capitalisation above 100 billion euros, of which the US has 79 and Europe has 20).

For years, the origins of these differences have been the target of studies by scholars, with several reasons emerging time after time: fragmentation, underdevelopment, limited access to finance by businesses (especially, SME’s and Startups), regulation and transparency barriers, with the occasional description of increased bank dependency in comparison to other regions, without forgetting the limited participation of EU households in capital markets versos their american counterparts, which should not come as a surprise, considering the differing levels of financial literacy across member states:

As the lack of a true European Capital Market has been evident for several years, it comes as no surprise that several initiatives had emerged in the past, such the Capital Markets Union (CMU) action plan of 2020, which had the goal of increasing the long-term investment horizons, kicked off as follow-up to the Banking Union created in 2014 in order to create a robust banking system and make way for a genuine economic and monetary union, but that was left incomplete and still in need for reform, though to disagreements by finance ministers.

The incompleteness of previous reforms and policies were complemented by the concerns raised on Enrico Letta’s report “Much More than a Market”, where the term of a Savings and Investments Union (SIU) seems to have been coined, and Mario Draghi’s report “EU Competitiveness : looking ahead”, providing support for pension system reform. Since then, the term Savings and Investments Union has been widely adopted by the European Commission, dotting every publication on the topic and public communications of the EU Commissioner, Maria Luís Albuquerque, and in the Commission’s public participation forum, totted as part of the strategy to reignite the clean energy’s sector with the € 650 billion it needs, alongside

Recommendations available

With the information obtained from public interventions of the EU’s Commissioner for Financial Services and Capital Markets Union, Maria Luís Albuquerque, as well as the over two hundred participations in the Commission’s public participation consultation, in which a multitude of companies and organizations representing the financial sector made a contribution (ranging from financial markets, hedge funds, national banking associations, national regulators, asset managers, academic institutions, national governments), a picture emerges of what a true Savings and Investment Union (SIU) could look like.

The strategy surrounding the SIU is likely to be based on four pillars:

- Citizens and Savings

- investment and financing

- Integration and Scale

- Efficient Supervision

To start, one of the targets clearly delineated by the Commission is to increase the participation of citizens as retail investors, seen as crucial in order to mobilize the 10 trillion euros said to be on low yield deposit accounts into the strategic areas requiring investment within the EU.

To do so, proposals include simplifying access to financial markets, improving financial literacy and reducing the regulatory costs of investment products, all of which become increasingly important in a world where ever growing volumes of information are made available and complicating the information processing abilities of a common retail investor. Such simplification of information is already being covered through the Retail Investment Strategy (RIS), aimed at standardizing the Key Information Documents to be provided to retail investors for easier comparison and facilitating the life of the institutions that commercialize them. However, national efforts for financial education improvement would still need to occur, adapted to the local realities, that could be supported by EU-level efforts (with standardized and easily comparable information), in order to minimize the disparities between the financial literacy rates among the citizens of member states and better prepare them as retail investors.

Additionally, to facilitate investment and investment by citizens, the creation of saving/investment accounts at EU level, based on successful models such as the Swedish ISK or the UK’s ISA, could be an option, as raised by Maria Luís Albuquerque, who also pondered the restructuring of the Pan-European Personal Pension Product (PEPP), in order to more closely resemble the american 401k model, in a more flexible and low-cost format. In alternative, a labelling of national financial products as fulfilling EU-level criteria could also emerge, though this would be below expectations and still restrictive to national dynamics.

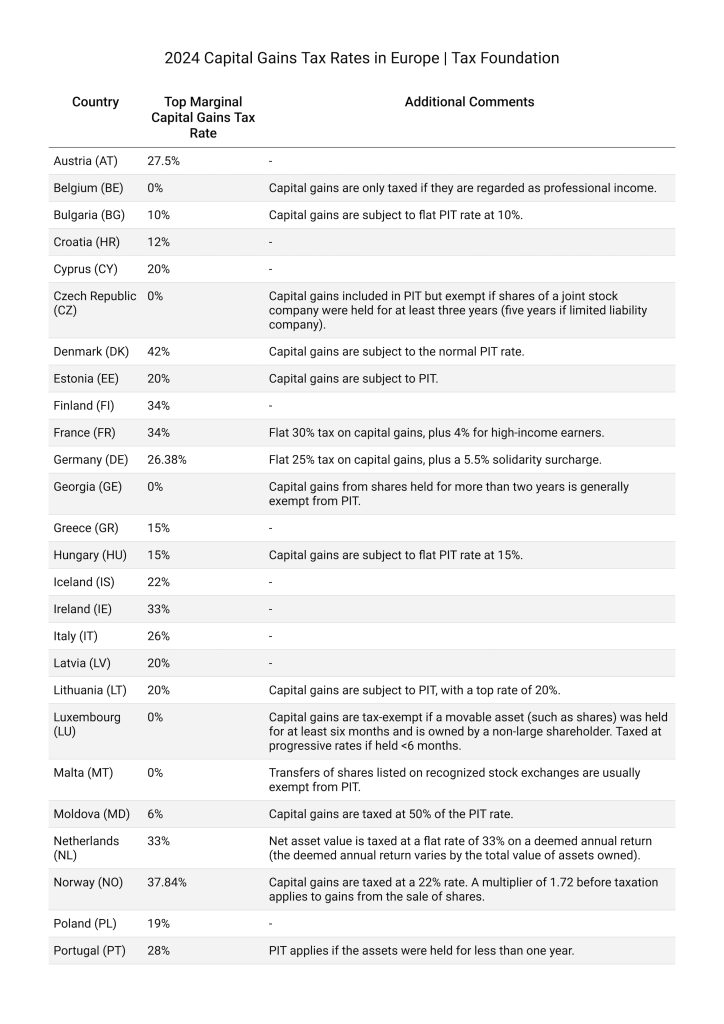

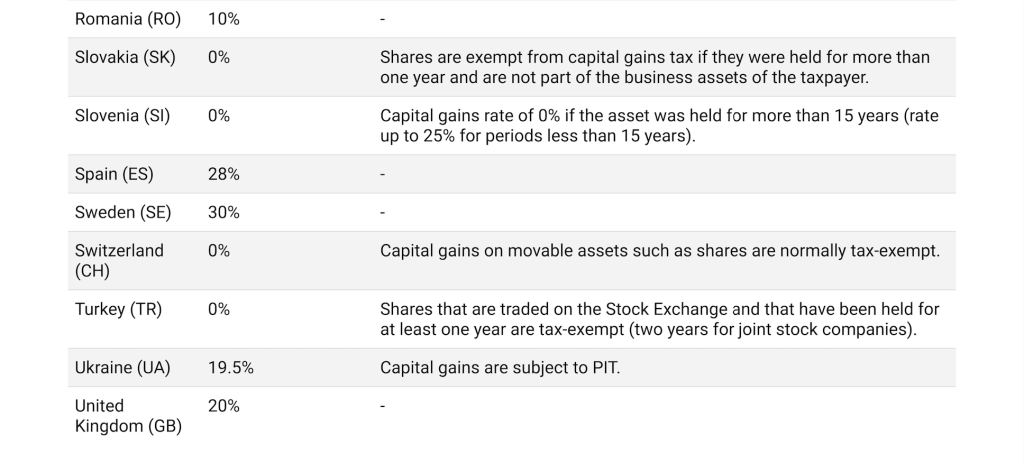

As also raised by the Commissioner, tax incentives ought to always be part of the equation offered by the member states, which, as one might expect, vary widely from country to country:

As observed, a better harmonization of capital gain taxes would benefit european citizens desiring to invest across the European Union, and ensuring freer movement of capital, essential for cross-border investment However, competition between countries, ideological debates and institutional egos are sure to make tax incentives a thorn into the implementation of the SIU.

Furthermore, directing new flows of investment and financing into the EU companies, especially SME’s and Startups, which often can’t depend only on bank credit, is a vital component of the future of the SIU, reinforced by the recommendations of the Letta report and the Draghi report, as well as part of the goals put forth by the recently launched “EU Startup and Scaleup Strategy”. To do so, the role of private capital markets and the revitalization of the european securitization (the conversion of an asset, especially a loan, into marketable securities, typically for the purpose of raising cash by selling them to other investors) could assist in improving the IPO ecosystem ( avoiding an outlook similar to that of the London Stock Exchange), while actually boosting the diversification of risk capital investment flows into new companies.

The mobilization of institutional investors is also vital in ensuring that improved flow of capital keeps the SIU’s aspirations within reach. Insurance and pension funds play a role in ensuring investment in equity markets, which was recently highlighted by Maria Luís Albuquerque, who argued that member states will be asked, under the SIU, to strengthen the pillar II and III of pensions (pillar I is Social Security; pillar II are pension funds and pillar III is voluntary and offers greater flexibility of choice). The Commission’s support for strong multi-pillar pension systems, on top of public, state, pensions, would assist on growing concerns of Social Security sustainability in a greying continent, while also injecting further capital into the European financial system. Yet, in an European Union built on higher expectations of the social security net, comparative to the US, the need to strengthen private participation for pension, though an inevitable topic, is also certain to involve discussions that should be approached pragmatically, as mentioned by the EU Commissioner.

In order to deliver on the potential scale up of the European financial markets, scalability of the European financial infrastructure is to also to be considered, including initiatives such as the completion of the Banking Union, including Single Supervisory Mechanism and of the Single Resolution Mechanism. However, it remains to be seen whether the wish to not put European banks (and financial institutions) at a disadvantage on the international stage due to competition laws/concerns will lead (national and/or) Competition authorities to be more strict on their opposal to acquisitions and mergers in the sector to further consolidate the sector, some of which seem to already be building up, with the moves of Italy’s Unicredit on Germany’s Commerzbank and the Dutch lender ING’s announced intention to acquire rivals, as well as those of financial markets operators, such as Euronext.

The ability to efficiently supervise all the new activity expected, as well as helping reduce existing capital market fragmentation, regulatory supervision is, without a doubt, a clearly important point. While the framework that sets the role of 3 European Supervisory Authorities (EBA – European Banking Authority; ESMA – European Securities and Markets Authority; EIOPA – European Insurance and Occupational Pensions Authority) is proposed to be reinforced and converged, recommendations are to be made that include potential transfer of national tasks to EU-level supervisors. While a stable, smooth and forward thinking policy and regulatory framework would be set to improve European financial markets, such a move of tasks is bound to be troubled, given the fees received by national supervisors, charged to those being supervised.

With better supervision, improved integration is more likely to assist in growth expectations across member states, independently from the size of their national financial markets, given that already large markets would have their size potential expand and small capital markets would see their companies have more capital potential within the European Union. Alongside this, the potential for the combination of EU bond emissions could prove to be a center-piece of the SIU, allowing for super secure, highly stable and secure assets, in high demand from institutional stakeholders, capable of competing with US Treasuries, even more if national issuances are made homogeneous. With such a decision, it would be possible to reinforce the role of the euro as an international reserve of value and allow the EU (and its member states) to better serve their geostrategic goals.

Finally, the application of the European capital targeted to be unlocked is to be promoted for strategic investments, such as the green transition, digitisation and defense. The widening of capital flow, if set alongside incentivizing tax treatment, can help improve the financing available for European companies that provide innovation in such areas, while providing clear frameworks on how sustainable finance can operate. In parallel, incentives to digitalization could also assist in making the financial markets themselves more easily accessible to Europeans across the European Single market, in a scenario where product subscription could be performed across digital borders, as well as more independent from the hegemony displayed, so far, but now fragilized, of US capital markets, through the investment in competitors (such as the case of potential competition to Paypal, MasterCard and VIsa, from a cross-EU joint venture).

The SIU Dream Unlocked

The complexity of capital markets, alongside the plurality of stakeholders involved, will make the successful implementation of the SIU an herculean task. Not only do capital markets include a tremendous number of areas across a pipeline of activities, all with their own key role, risking going unnoticed or neglected, but a fight due to national and regional interests is surely expected to happen, with political ideologies likely to influence pragmatic discussion on what could be a greater common goals.

However, despite the numerous obstacles, with the participation of stakeholders, hopefully triggered by the realization that greater growth and potential can be achieved by coming together on the chance to revise capital markets’ current infrastructure into a much smoother, open and dynamic framework, favorable to all those that believe in the essence of capital markets: allow for better allocation of capital in the economy.

The task of implementing the SIU will not be without its obstacles and it will require a wide array of ambitious initiatives and changes across the entire EU, but the prize on the table is too good to dare dream small.

Disclaimer: While Euro Prospects encourages open and free discourse, the opinions expressed in this article are those of the author(s) and do not necessarily reflect the official policy or views of Euro Prospects or its editorial board.

Write and publish your own article on Euro Prospects

Subscribe to our newsletter – stay informed when we publish articles on pressing European affairs.