20 min read — Long-Form Analysis | Economy | Trade | United States | EU

Tariff Wars: A Strategic Opportunity Brewing?

With the start of a second Trump presidency, a previously thought-to-be-buried trade strategy has reemerged: a tariff-first approach back on the table of EU-US trade relations.

By Nuno Dias Pereira — Finance Correspondent

Edited/reviewed by: Francesco Bernabeu Fornara

March 22, 2025 | 19:00

- The numbers

- The EU-US trade relationship

- How unbalanced is that?

- Can the tariffs’ impact be mitigated?

- What can we bring to the tariffs’ negotiation table?

- Can we become more independent from the US?

- Reflection

Long considered counterproductive to governments’ much-sought economic growth, protectionism has more often than not been sidelined as simply bad policy post-WWII.

Continuing a view already displayed in his previous administration, however, now-new US President Donald Trump has shown to preach protectionist policies, where any sort of trade imbalance unfavorable to the US is considered an affront—without considering any further macroeconomic factors, let alone consideration for alliances.

Were there need for any further evidence to back this claim, such stances have been widely proven by his repeated contentious takes on the US-EU trade relationship:

“”Look, let’s be honest, the European Union was formed in order to screw the United States,””

Notwithstanding, it is possible to empirically prove how these claims are made in an ill-informed vacuum— seemingly unwilling to recognize the multifactorial nature of trade wars and protectionism’s broader contex. And, arguably more importantly, it is likewise possible to strategize how the EU’s current trade deals may:

- mitigate a trade conflict with the US administration;

- fulfill its strategic independence and green goals with the change of external threats; and

- position itself as a leader in the global market as the US takes a step back.

In essence, the question plaguing European minds is whether the EU is equipped to counterbalance US tariffs and emerge stronger.

1. The numbers

Though quantitative facts have been sidelined by some (notably in the current US administration), what does the US–EU trade relationship actually look like?

- 1.1 The EU-US trade relationship

EU-US trade was shown to reach €1.5 trillion in 2023 as the sum of all imports and exports. However, two main categories within it should be focused on separately: trade of goods vs trade of services.

In goods, the EU has taken a stronger position, having exported, in 2023, €503 billion of goods to the US market, and imported €347 billion, translating into a trade surplus of €156 billion in goods for the EU that year. Does this mean that Donald Trump is in fact right in his criticisms? Well… partially.

When considering trade of services, the EU exported €292 billion worth of services to the US, while importing €396 billion, resulting in a services trade deficit of €104 billion for the EU.

In total, therefore, the aggregate balance of trade in goods and services between the EU and the US stood at €52 billion in 2023 (close to 54 billion in USD), to the EU’s favour, corresponding to a mere 3% of total trade between the two economic blocs.

- 1.2 How unbalanced is that?

In comparison, the trade of goods between the US and China ran a deficit (for the US) of $295 billion dollars in 2024. Additionally, US exports of services to China were an estimated $41.5 billion in 2022, while US imports of services from China were an estimated $26.6 billion in 2022, running a much more modest surplus for the US of $14,9 billion in services. As such, though data is not available for the same year, it’s possible to ascertain that the trade deficit between the US and China for 2022 in both goods and services stands at many times over that of the US–EU trade relationship.

Looking at closer trade partners, the US trade deficit of goods with Canada reached $63.3 billion in 2024 (but would have been a surplus if energy exports were to be excluded), with a US surplus in the trade of services closing to $12 billion in 2023.

In contrast, the US trade deficit of goods with Mexico reached $171.8 billion in 2024, with small surplus/deficits on the trade of services being observed in the last couple of years, the last of which found to be an US deficit of services trade reaching $ 630 million.

All this to show that, indeed, the EU runs a surplus of trade in goods with the US, but it runs a services deficit, while also not coming close to any of the other deficits run by the US with other trading patterns—if we are to take the simplistic view brought forth by the Trump administration.

But perhaps the EU has set up a tariff system that unfairly puts US goods at a disadvantage?

Again, the facts seem to disagree, with the USA itself confirming they have a trade-weighted average import tariff rate on industrial goods of 2.0%, while the EU’s weighted average is 1,37%. This actively puts into question the allegations in the White House’s memo that refers to the USA as having “the lowest average tariff rates in the world.”.

Considering the significance of bilateral trade between both blocs, it should come as no surprise that the implementation of tariffs would prove impactful.

2. Can the tariffs’ impact be mitigated?

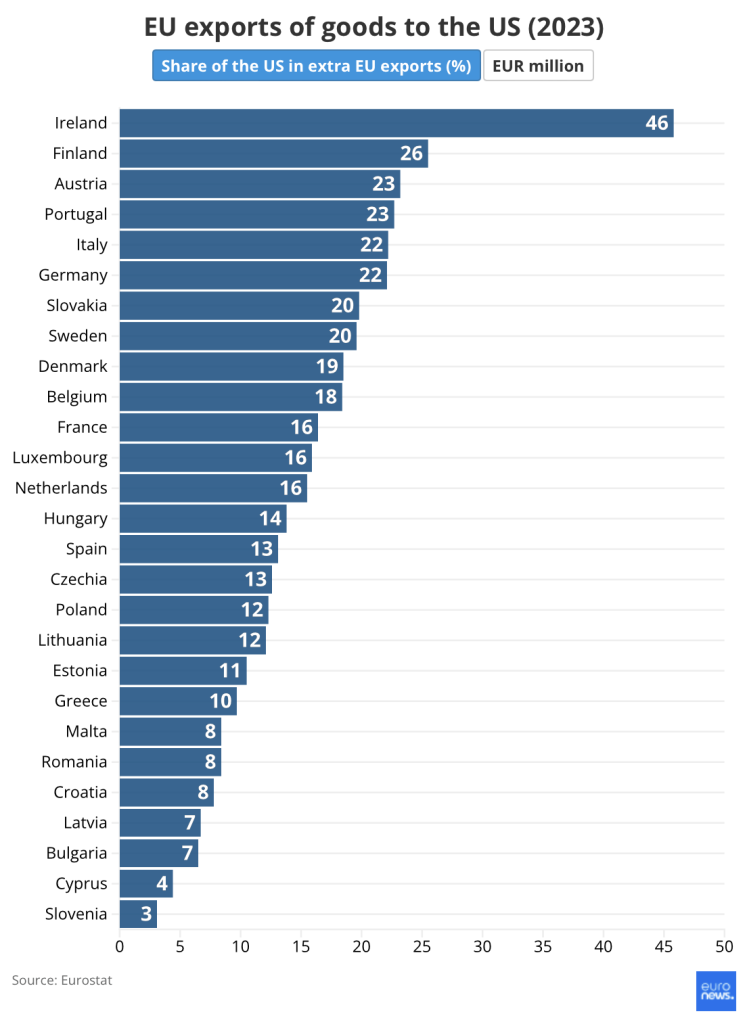

Of course, tariffs won’t impact all EU countries equally—not by a long shot. In order to truly assess the mitigation of the Trump-imposed tariffs’ impact, it’s important to reflect on the consequences that the tariffs might have on individual EU member states. As indicated in the graph below, the US generally represents a very significant market for nearly all member states’ extra-EU exports of goods:

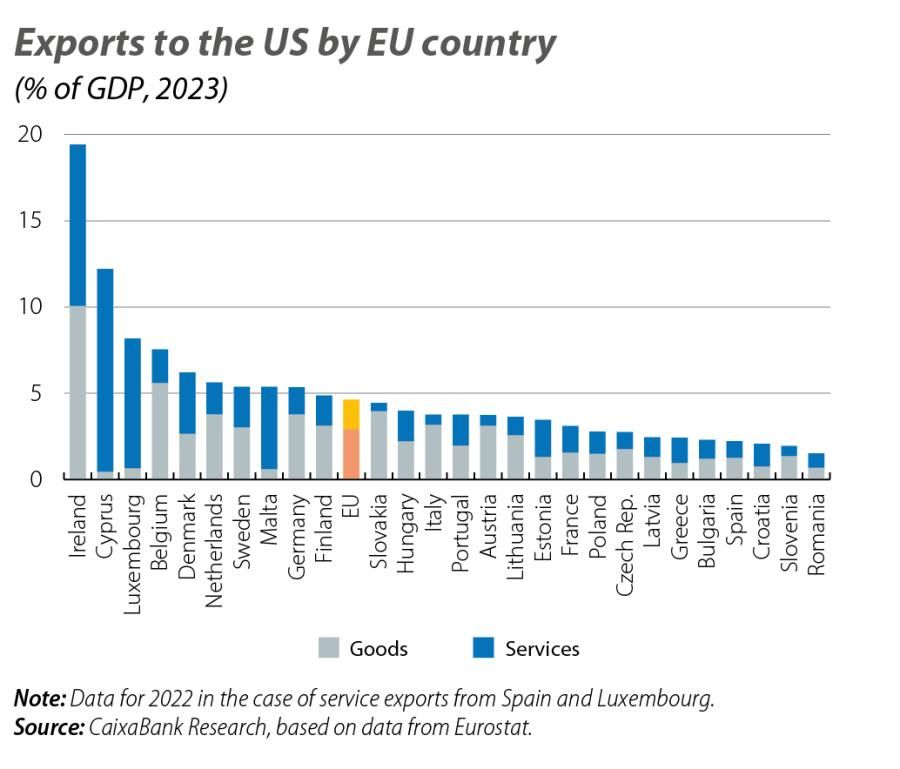

Furthermore, as analysed by Caixabank, based on 2023 data, the share of total exports that go to the US market, together with the degree to which an economy is trade-oriented, represents a significative percentage of all EU member states’ GDP:

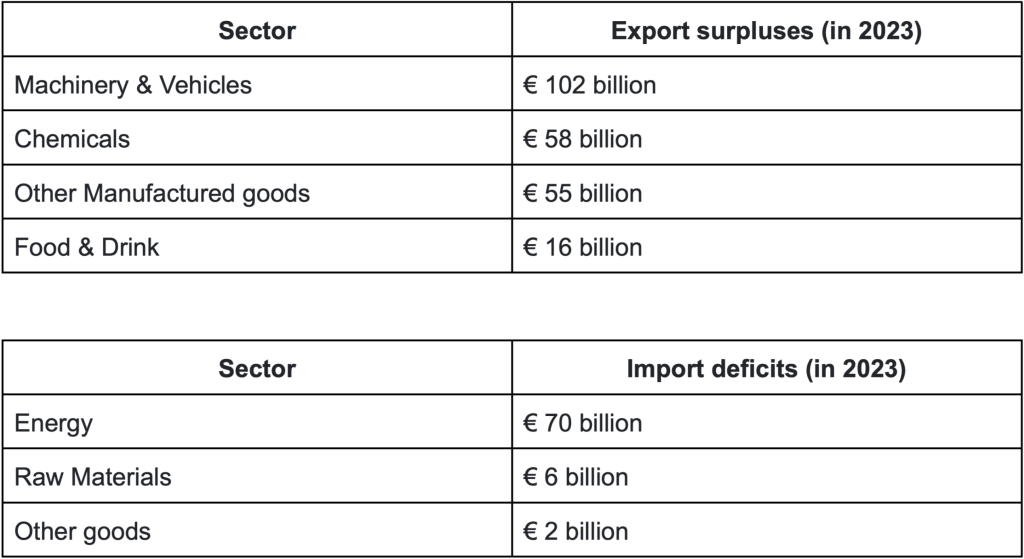

Naturally, each country has its own export/import balance with the US, with different industry sectors being more interconnected and dependent on said trade relations. However, from an aggregate perspective, the following sectors can be highlighted:

Given the percentages above, it’s no surprise that, to offset a likely drop in exports to the US, substitute markets would need to absorb the EU’s supply during a tariff war

As such, the proactiveness of the European Commission in negotiating a wide array of new trade agreements since the 2024 US Election will likely prove extremely useful.

In December 2024, the Mercosur trade agreement was revived, allowing the EU to further tap into a market to which its exports reach € 56 billion in goods (in 2023) and € 28 billion in services (in 2022). The agreement will protect EU interests by:

- Decreasing tariffs on critical raw materials and derived products; and

- Removing high tariffs for main EU export products (while also bringing an estimated € 4 billion in import barrier costs).

- In parallel, it will grant very limited access to the EU market for sensitive agri-food products like beef, poultry or sugar, and boost exports of agricultural and industrial goods, automobiles and pharmaceuticals to Latin America

In January 2025, the negotiations for a Global Agreement between the EU and Mexico were concluded, granting, primarily:

- Increased market access for agri-food exports, through the removal of 95% of high Mexican tariffs;

- Export restrictions removal on raw materials, including import duties, which will result in cheaper products; and

- Prohibiting export monopolies and unjustified government intervention in price setting

In February 2025, the EU Commission announced, during a trip to India, the goal to reach a free trade agreement by the end of year. Though such type of agreement has been delayed in the past, there are reasons to be optimistic:

- bilateral trade of goods between the EU and India reached € 124 billion in 2022-2023, alongside € 59.7 billion in trade of services in the same period.

- India signed a $ 100 billion free trade agreement with the European Free Trade Association (EFTA) in 2024

These are just some of the latest trade agreements or trade negotiations launched since a second Trump presidency was announced, not including older agreements that are just now coming into effect or other negotiations that have been announced since then, proving once again, that the US Administration’s claim of being “one of the most open economies in the world, and the lowest average tariff rates in the world” really falters when faced with reality.

However, the EU’s role of preparing for a tariff face-off with the US is not, and should not, be limited to merely replacing the US as the trade partner through other trade agreements.

The preparation must also include improvements to the EU’s own trade capabilities through internal improvements, something already recommended by the Competitiveness Report provided by Mario Draghi and resulting in the Commission’s proposed Competitiveness Compass, aimed at further reducing internal barriers, ensuring access to critical raw materials and capital financing.

Though implementing it will prove complicated and potentially controversial with trade partners due to its proposal for internal subsidies, it offers an opportunity to improve the efficiency and capability of Europe as a motor of trade and production.

With the increase of markets to which European goods and services can flow, as well as the increased efficiency of internal markets, the impact of tariffs coming from the US market could then be mitigated.

However, as seen above, the US market is simply too significant to be cut off without incurring severe negative impacts to all EU member states, underscoring the need for Europe to renegotiate and minimize the US tariffs imposed.

3. What can we bring to the tariffs’ negotiation table?

Firstly, a key consideration is to be taken into account: tariffs in the trade between developed nations is considered, as a rule of thumb, to be a lose-lose situation for everyone. Conversely, Trump has made his thinking clear, one where a transactional zero-sum game is to reign, with punitive tariffs as its primary means to do so.

Unlike the US, the EU can follow a more strategic course of action that doesn’t base itself on blankly applied retaliatory tariffs, bringing in a more savvy approach capable of managing the US’ blunt tantrum-like perspective.

In the first instance, appeal to the basic nature of trade. If the US wants to decrease their trade deficit with the EU, the EU should import more from the US. But what? Well, specifically, the things that the US wants to sell and that the EU, tactically, wants to buy: energy and arms.

Despite several rounds of sanctions and attempts at weaning Europe from the Russian energy sector, the EU continues to import energy from Russia. This is represented by the record 16.5 million metric tons of LNG obtained from Russia in 2024, surpassing the 15.2 million in 2023, with the total value of Russian fossil fuel imports reaching € 21.9 billion, higher than the € 18.7 billion spent in aid to Ukraine that same year. Considering the apparent dependence on Russian fossil fuels, what better way—while still struggling to decarbonise the European economy—to appease Trump’s “Drill Baby Drill” energy policy than to merely set up benefits to importing more energy resources from the US?

In parallel, as pleas for increased defense spending are made by European leaders, the European defense manufacturing industry is yet to break through its current capacity issues in the short-term at least, even though improvements have been made. Considering the ongoing growth of the EU-based defense sector, accompanied by increased defense spending, heightened defense purchases from the US could be used to argue in favor of easing tariffs on the manufacturing business, while the EU takes its time to find and grow their market share in other areas.

Finally, though diplomatic relations are always better suited for conflicts where negotiations are made in good faith, just like in nature, arson can be fought with strategically planned fires: retaliatory tariffs, on key sectors, that, though likely to cause its own issues to the EU-US trade relations, could help assist in the development of EU industries that are currently dependent on their US counterparts.

And taking a page from what were once some of the closest US allies, the EU could follow the Canadian example of specifically targeting the US states more closely aligned with the current US administration.

Nevertheless, the fact that such an intense trade situation has come to emerge, has led understandably to a reassessment of the economic dependency that the EU’s economy has developed when it comes to the USA.

4. Can we become more independent from the US?

As previously mentioned, in a globalized world, where free trade had been the norm, it can now seem complicated to untangle trade relationships as certain dependencies emerged.

However, with all the data available regarding trade, it is also possible to see the areas where more intense and potentially delicate dependencies can start being worked on. And, although complete entanglement would be very unlikely and troublesome, more independence can be achieved.

As mentioned previously, the EU incurs a deficit on the trade of services with the US, with increased exposure when compared with the trade of goods. The services’ category, regarding trade, can be broken into several subcategories, with the top three of EU trade being:

- Transport and auxiliary services – defined as the process of carriage of people and objects from one location to another as well as related supporting and auxiliary services (such as sea transport, air transport, etc)

- A type of service in which the US represents 14,5% of EU imports in 2022

- Travel Services – defined as goods and services for personal use or to give away, acquired from other economies by residents during visits to these other economies.

- A category in which the US represents 15.6% of extra-EU imports in 2022

- Business Services – defined to include R&D, legal services, accountancy and management consultancy, and real estate services

- A sector in which the US represented 35.1% of extra-EU imports in 2022

The connections with US companies of the service sector can be readjusted with specific initiatives and reforms.

For example, a Financial Markets and Savings Union, as proposed by the European Commission, could, hypothetically, allow for a bigger private sector investment in the EU economy, while withdrawing it from other markets, such as the US.

Such impact can be measured through data such as the € 9 382 billion in stocks abroad held by investors resident in the EU, 28% of which was absorbed by the US. Additionally, the clearly more conservative saving approach of EU citizens is observable, with a third of their savings being in deposits, when compared to the US counterparts, that have a tenth of their savings in deposits. By making investment and saving products more standardized and appealing across Europe, more money could be brought from abroad and from within into the EU’s economy, assisting in the financing of its proposed investments and the desired independent and competitive industries.

Additional capital market liquidity is becoming increasingly needed, as it has become clear from the US president’s intervention, the administration seems to operate under a logic of prowess, claiming that Ukraine has survived thanks to the US and that Europe has loaned (and retrieved said loans) from Ukraine. This argument falters when faced with the facts, such as:

- Since 2022, the difference between US and European (EU + UK) support to Ukraine was $ 64 billion to $ 62 billion

However, the diminishing US capability to assist Europe in military defense, while also targeting it with tariffs, make the great case for the European military defense industry to thrive while protected from its American counterpart. As highlighted previously, the purchase of additional military equipment can be used to dangle a carrot to the US administration.

However, with the direction followed by the US, the supply quality and price can no longer be taken as assured, considering the constant looming of tariffs, which becomes particularly concerning considering that between mid-2022 and mid-2023, 63% of all EU defense orders were placed with US companies.

In 2024, the US approved a military budget of $ 824 billion and $ 150 billion in defense research and development spending, while the EU’s aggregated military budget estimates reached € 326 billion and a meager €10.7 billion euros in defense research.

However, if the EU members were to match the 2% of GDP NATO military budget commitment (without including the UK), under the 2024’s estimates of a $ 19.7 trillion GDP, it would reach a $ 394 billion military budget, with much of that potentially becoming available for EU firms, in addition to the billions that could be weaned off from the US Military complex, as well in savings that could be brought forth by a stronger European Defense Union making common purchase orders. This boon in technological investment for defense could also be accompanied by a boost to space and telecommunications’ investments that would bring strategic independence from US technology, such as the replacement of the Starlink reliance, using its own technology.

The reform of capital markets, alongside higher investment in technological investment associated with the defense sector, could also contribute, alongside additional measures, to a virtuous cycle regarding innovation in the EU.

Despite the EU’s increasing, yet still lower than the US, innovation output indicator , it still lags behind the US and China when it comes to investment in research and developments, focused on small continuous improvements in traditional sectors such as automotive manufacturing instead of breakthrough scientific areas.

Such stifling of innovation, in addition to the reforms and investments already mentioned, could be also be improved by making structural changes to the funding of projects, such as replacing the current civil servants at institutions such as the European Innovation Council (EIC) with actual experts on the fields for which funding is being requested, with, of course, proper compliance supervision.

In parallel with higher investment, EU projects to reform the european academia, like the idea of European degrees (taught across European universities), could prove useful to attract US scientists aiming to escape and thrive despite the attempted persecution so swiftly implemented in the US scientific community, where articles on topics deemed controversial by the administration were pulled, researchers left without their funding, all of which allowing the EU to emerge as a greener pasture than the now unstable US universities].

5. Reflection

Despite the current US administration’s apparent incapability to recognize factual economic data or nuance, instead opting for hammering their own choices into the rest of the world’s economy, that does not mean that all their trade partners (either allies or frenemies) are meant to take it lying down.

The global economic order is changing, disregarding what had been a contemporary history of mutual respect and diplomacy based on the rules-based international order, painted with a broad consensus around the expectations of free(r) trade. It has become clear, though, that a multipolar geopolitical status quo is emerging, pushing Europe to stand on its own ground, with alliances becoming more punctual and less reliable.

To stand its own ground, the EU and its members are not without options, but must take bolder, more proactive, ambitious and flexible action, disregarding the expectations previously set within the traditional transatlantic relationship. Europe should now set itself as the key trade player it has always been foretold to be, but has, so far, failed to live up to its full potential.

The EU is able to learn, adapt and rise to the occasion as we’ve seen in the last graceless and classless episodes emerging from the US. It just has to do it faster and better.

Disclaimer: While Euro Prospects encourages open and free discourse, the opinions expressed in this article are those of the author(s) and do not necessarily reflect the official policy or views of Euro Prospects or its editorial board.

Write and publish your own article on Euro Prospects

Subscribe to our newsletter – stay informed when we publish articles on pressing European affairs.